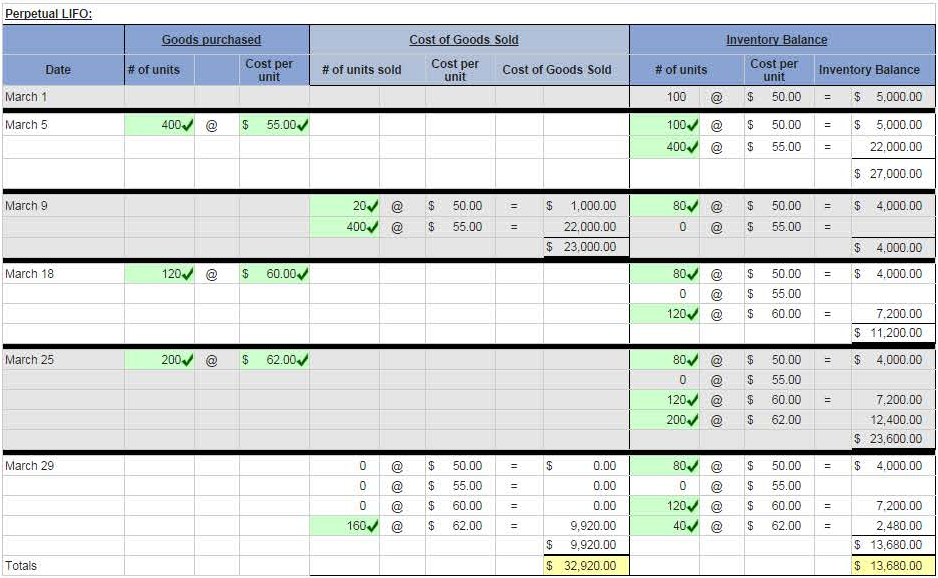

Thus, after two sales, there remained 75 units of inventory that had cost the company $27 each. Ending inventory was made up of 75 units at $27 each, and 210 units at $33 each, for a total FIFO perpetual ending inventory value of $8,955. At the time of the secondsale of 180 units, the FIFO assumption directs the company to costout the last 30 units of the beginning inventory, plus 150 of theunits that had been purchased for $27. Thus, after two sales, thereremained 75 units of inventory that had cost the company $27 each.The last transaction was an additional purchase of 210 units for$33 per unit.

The company uses a periodic inventory system to account for sales and purchases of inventory. It has grown since the 1970s alongside the developmentof affordable personal computers. Universal product codes, commonlyknown as UPC barcodes, have advanced inventory management for largeand small retail organizations, allowing real-time inventory countsand reorder capability that increased popularity of the perpetualinventory system.

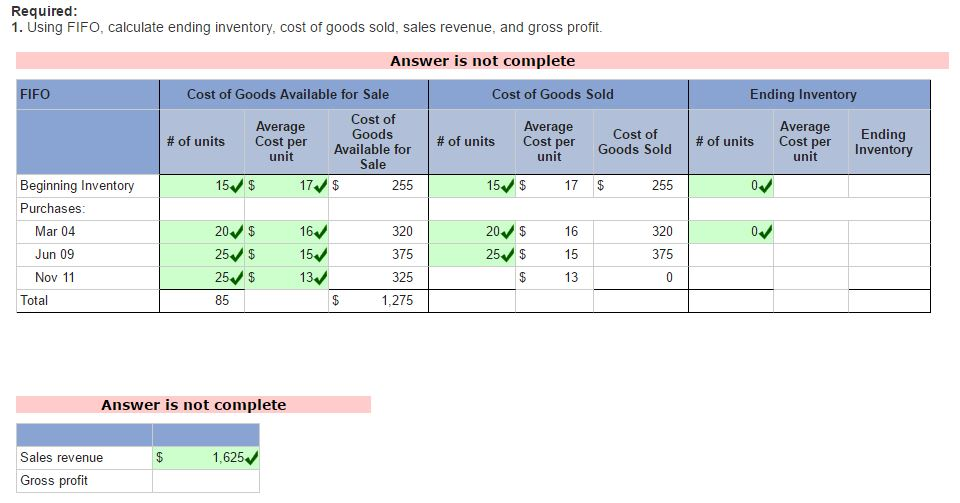

At its most basic level, ending inventory can be calculated by adding new purchases to beginning inventory, then subtracting the cost of goods sold (COGS). Advancements in inventory management software, RFID systems, and other technologies leveraging connected devices and platforms can ease the inventory count challenge. Figure 10.14 shows the gross margin, resulting from the specific identification perpetual cost allocations of $7,260. When calculating the Cost of Goods Sold for a sale, you must IGNORE the selling price.

For a firm to calculate the total cost of its ending inventories, it is first necessary to determine the actual quantity of items in the ending inventory and then to attach a price to these items. This represents the total value of sellable inventory at the end of the accounting period. For each item in inventory, determine the unit cost based on the chosen inventory valuation method (e.g., FIFO, LIFO, weighted-average). To calculate ending inventory, you need to know the value of the beginning inventory at the start of the accounting period.

The ending inventory under LIFO would, therefore, consist of the oldest costs incurred to purchase merchandise or materials inventory. If all items are purchased at the same price, there will be no problem in determining the cost of either the ending inventory or the items sold. For retailers, this means that acquisition costs include the purchase price less any sales discounts, plus other freight charges, insurance in transit, and sales taxes that are incurred to have the product ready for sale. This is usually done by taking a physical inventory at least once a year, usually at year-end. A physical inventory is required, regardless of whether a firm uses the perpetual or the periodic inventory method.

It is important to note that these answers can differ when calculated using the perpetual method. When perpetual methodology is utilized, the cost of goods sold and ending inventory are calculated at the time of each sale rather than at the end of the month. For example, in this case, when the first sale of 150 units is made, inventory will be removed and cost computed as of that date from the beginning inventory. The differences in timing as to when cost of goods sold is calculated can alter the order that costs are sequenced.

This ratio is then applied to the net sales during the accounting period to estimate the cost of goods sold. Subtracting the estimated cost of goods sold from the cost of goods i filed an irs return with the wrong social security number available for sale gives the estimated ending inventory. Figure 10.14 shows the gross margin, resulting from thespecific identification perpetual cost allocations of $7,260.

Let’s return to The Spy Who Loves You Corporation data to demonstrate the four cost allocation methods, assuming inventory is updated on an ongoing basis in a perpetual system. On December 31, 2016, a physical count of inventory was made and 120 units of material were found in the store room. The Meta company is a trading company that purchases and sells a single product – product X. The company has the following record of sales and purchases of product X for the month of June 2013.

The first-in, first-out method (FIFO) of cost allocation assumes that the earliest units purchased are also the first units sold. For The Spy Who Loves You, using perpetual inventory updating, the first sale of 120 units is assumed to be the units from the beginning inventory, which had cost $21 per unit, bringing the total cost of these units to $2,520. At the time of the second sale of 180 units, the FIFO assumption directs the company to cost out the last 30 units of the beginning inventory, plus 150 of the units that had been purchased for $27.